Newsletter - August 19th, 2023

- AuditorInvestor

- Aug 19, 2023

- 2 min read

Dear Reader,

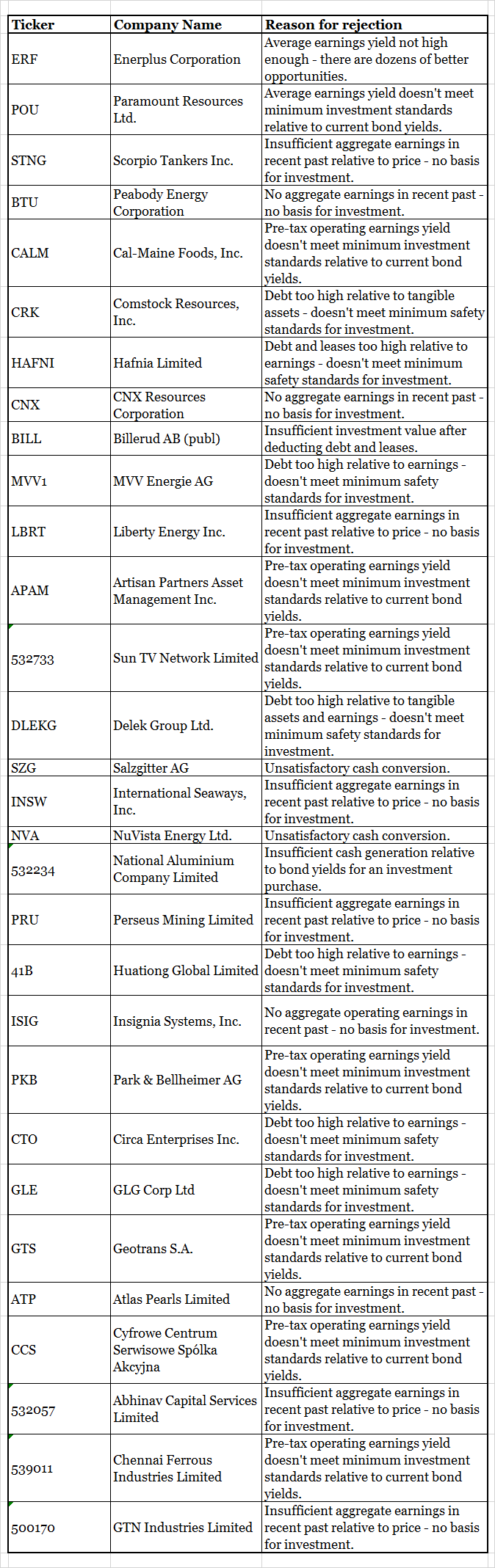

Attached is our latest list of stocks generated from basic value screens (low p/e, ev/ebitda, debt/equity, etc.), which don’t meet our investment criteria - and our reasoning.

This may help you avoid a few ‘value traps’ or stocks that aren’t sufficiently attractive compared to the opportunities available today.

For reports of stock ideas that pass our quantitative and qualitative standards, join at the link below: